All Categories

Featured

Table of Contents

Juvenile insurance coverage may be marketed with a payor advantage biker, which supplies for waiving future costs on the youngster's plan in the event of the fatality of the person that pays the costs. what is a renewable term life insurance policy. Elderly life insurance policy, in some cases referred to as rated survivor benefit plans, gives eligible older candidates with very little whole life coverage without a medical exam

The optimum issue amount of insurance coverage is $25,000. These plans are typically much more expensive than a totally underwritten plan if the individual certifies as a basic risk.

You choose to obtain one year of highly inexpensive protection so you can determine if you want to commit to a longer-term plan.

The Federal Government developed the Federal Personnel' Team Life Insurance Coverage (FEGLI) Program on August 29, 1954. It is the largest team life insurance program worldwide, covering over 4 million Federal staff members and senior citizens, in addition to several of their household members. The majority of employees are qualified for FEGLI coverage.

Guaranteed Level Premium Term Life Insurance

Because of this, it does not develop any money worth or paid-up worth. It includes Basic life insurance coverage and 3 options. In most cases, if you are a new Federal worker, you are immediately covered by Standard life insurance policy and your payroll workplace subtracts costs from your paycheck unless you forgo the coverage.

You must have Fundamental insurance coverage in order to choose any of the choices. The expense of Standard insurance is shared between you and the Federal government.

You pay the full expense of Optional insurance, and the price relies on your age. The Office of Federal Worker' Team Life Insurance (OFEGLI), which is a personal entity that has an agreement with the Federal Government, processes and pays insurance claims under the FEGLI Program. The FEGLI Calculator permits you to figure out the stated value of numerous mixes of FEGLI insurance coverage; compute premiums for the numerous mixes of protection; see exactly how choosing various Choices can transform the amount of life insurance and the premium withholdings; and see how the life insurance policy brought right into retirement will certainly alter over time.

Term life insurance policy is a kind of life insurance that provides insurance coverage for a specific period, or term, selected by the insurance policy holder. It's generally one of the most straightforward and cost effective life insurance option by covering you for an established "term" (life insurance policy terms are commonly 10 to 30 years). If you pass away during the term duration, your recipients receive a cash money payment, called a death advantage.

Term life insurance policy is a straightforward and cost-effective solution for people looking for economical defense during particular periods of their lives. It is necessary for people to carefully consider their monetary goals and needs when picking the duration and amount of coverage that best fits their situations. That said, there are a couple of reasons that many individuals pick to get a term life plan.

This makes it an eye-catching choice for people that desire considerable insurance coverage at a lower price, particularly during times of greater economic responsibility. The other vital benefit is that premiums for term life insurance policy policies are repaired for the period of the term. This suggests that the insurance policy holder pays the same costs amount each year, providing predictability for budgeting objectives.

Short-term Life Insurance

1 Life Insurance Policy Statistics, Information And Sector Trends 2024. 2 Price of insurance coverage rates are determined making use of approaches that vary by firm. These prices can vary and will normally raise with age. Prices for energetic workers might be various than those readily available to terminated or retired employees. It is necessary to consider all factors when reviewing the general competitiveness of rates and the worth of life insurance protection.

Like the majority of group insurance policy policies, insurance coverage policies supplied by MetLife consist of specific exclusions, exceptions, waiting periods, reductions, restrictions and terms for keeping them in pressure. Please call your advantages administrator or MetLife for prices and complete details - accidental death insurance vs term life.

Our term life options consist of 10, 15, 20, 25, 30, 35, and 40-year policies. One of the most popular type is level term, meaning your payment (premium) and payment (fatality advantage) remains level, or the exact same, until completion of the term duration. This is the most simple of life insurance policy alternatives and calls for really little upkeep for plan proprietors.

You could provide 50% to your partner and divided the rest amongst your adult children, a parent, a pal, or also a charity. * In some circumstances the survivor benefit might not be tax-free, find out when life insurance coverage is taxable.

Term life insurance policy supplies coverage for a details time period, or "term" of years. If the guaranteed individual dies within the "term" of the plan and the plan is still active (energetic), then the survivor benefit is paid to the beneficiary. best decreasing term life insurance. This type of insurance policy commonly enables clients to at first buy more insurance policy protection for much less cash (premium) than other sort of life insurance policy

Life insurance acts as a replacement for earnings. The potential threat of shedding that gaining power earnings you'll need to fund your household's greatest goals like getting a home, paying for your youngsters' education and learning, lowering financial obligation, conserving for retired life, and so on.

Term Life Insurance Policy Matures When

Term life is the most basic form of life insurance policy. If you acquire term life insurance at a more youthful age, you can generally acquire even more at a reduced cost.

Term insurance is ideally matched to cover certain demands that may reduce or go away over time Complying with are two typical stipulations of term insurance plan you may desire to think about throughout the purchase of a term life insurance policy plan. allows the guaranteed to renew the policy without having to verify insurability.

Before they offer you a policy, the service provider needs to analyze exactly how much of a danger you are to insure. This is called the "underwriting" procedure. They'll normally request for a medical exam to assess your wellness and want to understand even more about your line of work, lifestyle, and various other things. Certain hobbies like scuba diving are deemed high-risk to your wellness, which might elevate rates.

Term Life Insurance As Collateral For A Loan

The prices linked with term life insurance coverage costs can differ based on these variables - what is a term rider in life insurance. You need to choose a term size: Among the most significant questions to ask yourself is, "How much time do I need protection for?" If you have children, a prominent general rule is to choose a term enough time to see them away from the house and with college

1Name your recipients: Who obtains the advantage when you die? It doesn't all have to go to a single person. You can offer 50% to your spouse and divide the rest between your adult youngsters. And while beneficiaries are commonly family members, they don't have to be. You might pick to leave some or all of your benefits to a trust fund, a philanthropic organization, or perhaps a good friend.

Take Into Consideration Making use of the DIME formula: penny represents Financial obligation, Revenue, Mortgage, and Education and learning. Complete your debts, home loan, and college expenses, plus your income for the variety of years your family members needs defense (e.g., until the children run out the home), and that's your insurance coverage demand. Some economic specialists calculate the amount you need utilizing the Human Life Worth ideology, which is your life time earnings potential what you're gaining now, and what you anticipate to earn in the future.

One means to do that is to look for companies with solid Economic toughness ratings. 8A firm that finances its very own policies: Some business can market policies from one more insurance firm, and this can add an added layer if you want to transform your plan or down the road when your household requires a payout.

Some business provide this on a year-to-year basis and while you can anticipate your prices to rise significantly, it may deserve it for your survivors. An additional way to compare insurer is by checking out online client testimonials. While these aren't likely to tell you much regarding a company's economic security, it can tell you how easy they are to function with, and whether insurance claims servicing is an issue.

What Is Term Rider In Life Insurance

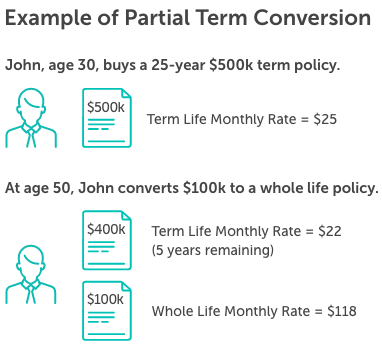

When you're younger, term life insurance policy can be an easy means to safeguard your loved ones. As life modifications your economic top priorities can as well, so you may desire to have whole life insurance policy for its life time coverage and extra benefits that you can utilize while you're living. That's where a term conversion is available in.

Authorization is assured despite your wellness. The costs won't enhance once they're established, but they will increase with age, so it's a good concept to secure them in early. Figure out even more regarding exactly how a term conversion works.

1Term life insurance policy uses temporary protection for an essential duration of time and is normally more economical than irreversible life insurance policy. 2Term conversion standards and restrictions, such as timing, might use; for instance, there may be a ten-year conversion opportunity for some products and a five-year conversion privilege for others.

3Rider Insured's Paid-Up Insurance Acquisition Alternative in New York City. 4Not offered in every state. There is a price to exercise this cyclist. Products and riders are offered in authorized jurisdictions and names and attributes might vary. 5Dividends are not assured. Not all taking part policy owners are qualified for dividends. For select riders, the problem puts on the guaranteed.

{kind=link}

Latest Posts

15 Year Level Term Life Insurance

What Is Level Term V Life Insurance

How Does Decreasing Term Life Insurance Work